Reading Time: 3 minutes

New Year’s resolutions typically focus on healthier lifestyles, kicking bad habits, and ways to increase happiness. Unfortunately, there’s a tendency to drop resolutions as quickly as they’re started – on average, most don’t make it to January’s end. K·Coe tax advisors are putting an end to the resolution let-down by providing some sure-fire tax resolutions that are fairly simple to employ now, and will leave a rewarding result throughout the year:

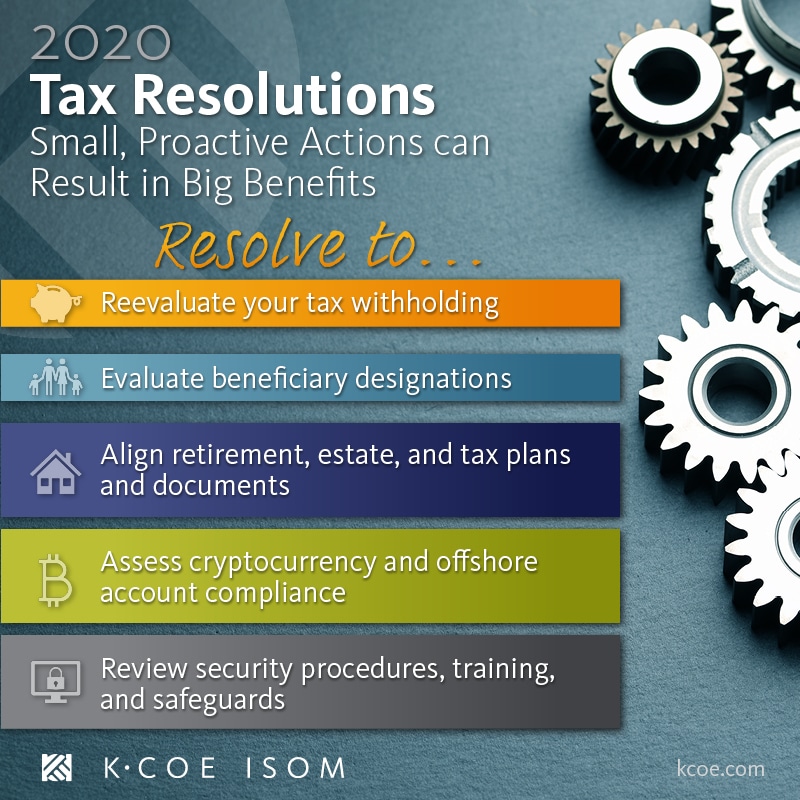

Is Your Tax Resolutions Plan 2020 Ready?

- Do you know if you’re withholding too much or too little tax? Make sure you’re on the right course by doing a withholding check-up in advance. It’s important because this simple check can alert you to potential changes needed on a Form W-4. You especially want to assess this if you’re expecting a significant life change (buying a house, getting married, having a baby) in the new year. The new Tax Cuts and Jobs Act (TCJA), also known as tax reform, might also impact your tax withholding this year.

- Resolve to reevaluate your tax withholding. Use the IRS’ Tax Withholding Estimator, or contact your tax advisor.

- When was the last time you reviewed beneficiary designations? While the recommendation is to review these annually, the reality is that people typically fill them out the first time and don’t revisit them unless required. Recent retirement regulation changes under the newly-signed SECURE Act of 2019 may impact how taxpayers and their beneficiaries now contribute to and benefit from retirement and other accounts.

- Resolve to evaluate beneficiary designations on retirement accounts, life insurance, and other non-probate assets.

- Has your estate plan been adjusted to reflect new changes? Beneficiary designations, non-probate assets, and increased federal estate exemption amounts should all be adjusted and properly reflected within estate planning documents. In addition, marital and family trusts may not be applicable any longer, or might require greater flexibility. Lastly, trusts which incorporate IRA provisions might need revisions under the new SECURE Act regulations. Significant life changes and income tax planning rearrangements (for example, converting a second home to a business) will need adjustments as well.

- Resolve to confirm that retirement strategies are aligned with overall estate and tax planning goals, and that all changes are being reflected in estate planning documents.

- If you use cryptocurrency or offshore accounts, have you taken the steps necessary to become and remain compliant? With the IRS’ focus on cryptocurrency in the coming year, and the addition of a checkbox on Schedule 1 of Form 1040 which indicates a taxpayer’s financial interests in virtual currency, it is important to be extra vigilant and proactive in these areas. Failure to answer those questions, or answering them incorrectly, can have serious consequences and damaging civil and criminal penalties.

- Resolve to discuss cryptocurrency and offshore accounts, and the steps needed to become and remain compliant, early this tax year.

- Are you protected from identity theft and identity theft-related tax fraud? Be careful not to assume the answer is yes – financial and tax data security is a priority throughout the year which needs to be tended to. Under the IRS, tax professionals are under strict guidance to have data protection plans and protect client data. Security plans cannot be fully protective if they are only one-sided, and therefore taxpayers are also advised to make data security a priority.

- Resolve to check entry points, update security training, review procedures, create strong passwords, avoid public WIFI connections when transmitting or accessing sensitive financial data, and use care when discussing financial and tax accounts.

Making these resolutions early every year can provide a checks-and-balances system for the benefit of taxpayers – ensuring that you are meeting compliance regulations and maximizing all available tax benefits under the most current regulations.